An Update on Inflation

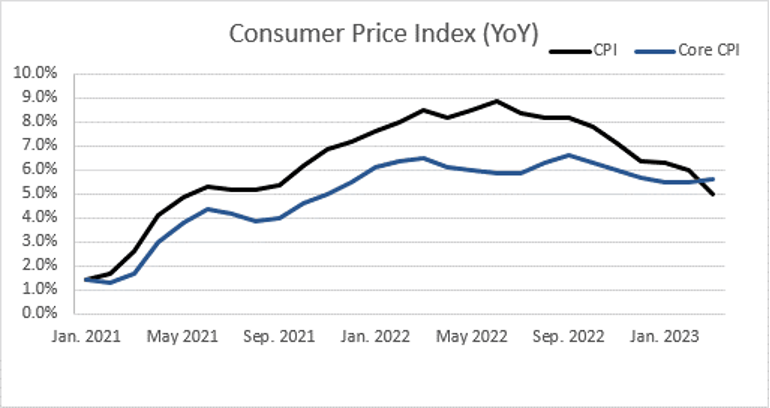

Consumer Price Index (CPI) Inflation decreased in March. Headline inflation in March slowed to +5.0% and Core CPI came to +5.6% on an annualized basis. On a month-over-month basis, CPI rose +0.1%, half of what was expected, while Core CPI rose a higher +0.4%, on track with estimates.

Remember that Core CPI removes the impact of energy and food prices, which are typically more volatile, from the data.

Most notably, transportation services, electricity, and shelter drove inflation higher, while energy and used cars drove inflation lower from a year ago. Compared to February, food at home prices (as opposed to eating out) fell -0.3% in March, a great help to consumers when they stock their fridges.

Producer Price Index (PPI) decreased even more. Often thought of as a leading indicator of inflation, PPI was lower in March, with PPI up +2.7% and Core PPI up +3.6% on an annual basis. Month over month, PPI fell a rapid -0.5% from February, compared to 0.0% inflation expected, while Core PPI rose as expected at +0.3%.

Similar to Core CPI, the Core PPI measures the impact of price increases on producers of goods minus the impact of more volatile energy and food prices.

We believe that PPI and CPI reports that were below expectations are a good sign that will help to reduce the likelihood of multiple Fed interest rate increases in the coming months. However, the Fed’s work is not done. The real test of inflation comes in a few weeks when March’s Personal Consumption Expenditures (PCE) Price Index is reported. PCE is the Fed’s preferred inflation metric. The good news is that we expect PCE to follow the trends of CPI and PPI, as these inflation metrics provide strong comparable data on inflationary pressures prior to the PCE report.

Looking Ahead

Last week we saw CPI decrease to a still higher than wanted +5.0% inflation rate in March, while PPI decreased even more to +2.7%. We also saw that retail sales slowed in March and the first week of initial jobless claims in April showed an upward trend.

Based on this data, it appears that the Fed’s increase in interest rates may be starting to impact input prices and the performance of the economy. However, the real difficulty lies ahead. The Fed will need to continue to convince consumers and financial markets that it will do what is necessary to reduce inflation while not being so aggressive that it causes a recession. Given the difficulty of threading this economic and financial needle, we expect uncertainty and volatility to persist. Therefore, we will continue to be defensive in our investment allocation and hold more cash than typical so we can take advantage of opportunities that arise because of emotional overreactions to short-term data.